For high-net-worth investors and retirees seeking to refine their portfolios in 2025, the debate between direct indexing and ETFs is no longer merely academic.

Indeed, with recent innovations in tax optimization and personalized investing, direct indexing is rapidly becoming a practical alternative to traditional index-based strategies that once dominated the investment discourse for everyday retail investors.

But is direct indexing right for you?

This article breaks down the key differences between direct indexing and ETFs, explores the benefits of each, and explains how HUDSONPOINT capital can help tailor a solution aligned with your financial goals.

What Is Direct Indexing?

The goal of direct indexing is to replicate an existing market benchmark or index, such as the S&P 500 or theNasdaq, by owning the individual stocks that comprise the index, typically through a separately managed account (SMA).

Unlike buying shares of an ETF or mutual fund that are managed by a third party, direct indexing provides investors with fractional or full ownership of the underlying securities. This structure opens the door to deeper customization and enhanced tax management, particularly via tax-loss harvesting.

When done properly, direct indexing can deliver greater after-tax returns, especially for high-income investors, by systematically harvesting losses and reducing capital gains tax exposure throughout the year.

Direct Indexing vs. ETFs: By The Numbers

A simulation comparing an S&P 500 direct index portfolio with the SPDR S&P 500 ETF (NYSE: SPY) from 2003–2013 showed that direct indexing boosted after-tax annual returns by more than 2% (assuming a high 42.3% tax rate), excluding advisory fees.

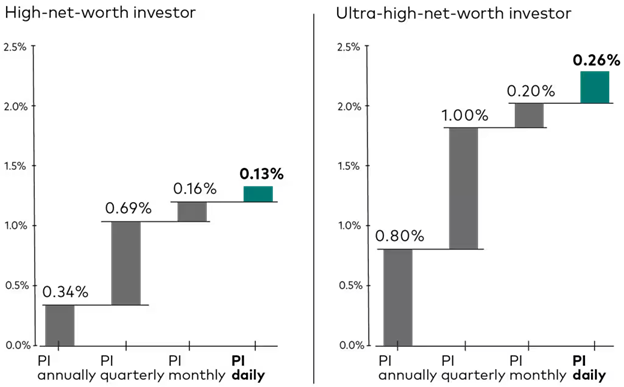

Vanguard data also suggests that proper direct indexing strategies can offer enhanced after‑tax returns by 1% to 2% annually due to systematic tax-loss harvesting. For example, the S&P 500 gained 11.7% in Q4 2023, yet 178 individual equities in the SPY ETF lost value during that time.

For everyday retail investors, harvested losses can be used to offset up to $3,000 of ordinary taxable income from capital gains, and losses can also be carried forward to future years. Notably,the savings from tax-loss harvesting can be even greater for high-net-worth and ultra-high-net-worth investors.

Source: Average 10-year TLH alpha by harvest frequency (Vanguard)

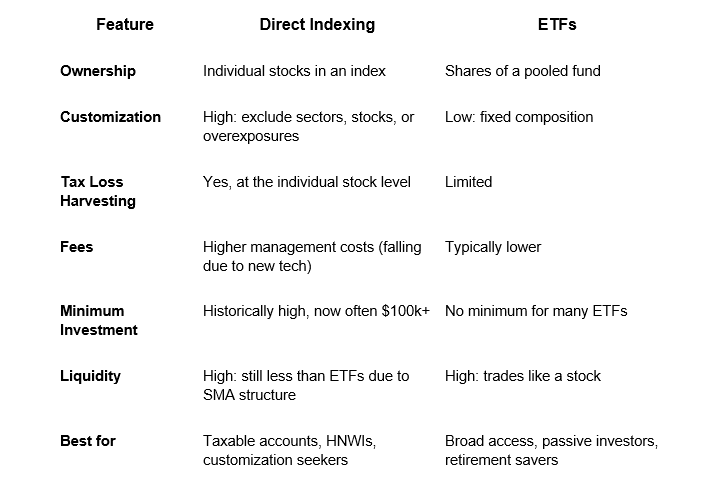

Direct Indexing vs. ETFs: A Side-by-Side Analysis

Direct indexing provides investors with actual ownership of individual stocks, which opens the door to tax-loss harvesting and portfolio personalization that pooled ETFs simply can't match.

The ability to exclude specific sectors or individual equities makes direct indexing especially attractive for investors who want to align their portfolios with personal values or reduce risk exposure from over-concentrated holdings.

Of course, this degree of control comes at a cost. Good luck trying to directly index to a benchmark on your own. And if you ask a firm to help you with a direct indexing strategy, it typically comes with higher fees and requires a larger minimum investment.

The Case For Direct Indexing

Direct indexing is gaining traction for good reason. One of its most compelling advantages is the potential for tax optimization through individualized tax-loss harvesting. By selectively selling losing positions throughout the year, investors can offset gains elsewhere in their portfolio, effectively reducing their overall tax liability. This strategy is particularly valuable for those in higher tax brackets, where even incremental tax savings can compound meaningfully over time.

Beyond taxes, the power of customization cannot be overstated. Investors are increasingly seeking to have their portfolios reflect their personal values—whether that involves avoiding fossil fuels, reducing exposure to technology, or emphasizing diversity and inclusion. Direct indexing permits this level of personalization without sacrificing the diversification of an index.

Finally, for investors with sizable positions in specific stocks (perhaps acquired through executive compensation or long-term holdings), direct indexing allows for more targeted, surgical portfolio construction, avoiding overexposure to any single name or sector.

The Drawbacks of Direct Indexing

While the appeal of direct indexing is strong, it’s not without its trade-offs. Cost remains a barrier for some investors. Although fees have fallen significantly as the market continues to mature, direct indexing accounts often still incur advisory, custodial, and transaction-related expenses that can exceed those of low-cost ETFs.

Complexity is another consideration. Customizing a portfolio at the individual stock level and implementing an on going tax strategy requires a disciplined, active management approach. Investors who prefer a more hands-off experience may find this daunting unless they work with a qualified advisor.

While access is improving, many direct indexing platforms still require steep minimum investments, sometimes in the millions. This makes direct indexing more appropriate for affluent investors or those managing multiple taxable accounts with sufficient capital.

How HUDSONPOINT capital Can Help

Direct indexing is a powerful tool for refining and optimizing your investment strategy with precision. But exclusive institutional-level direct indexing solutions, such as BlackRock’s Aperio and Vanguard Personalized Indexing, only appeal to more affluent clientele.

As direct indexing grows, so do platforms offering solutions tailored to a range of investor needs. Some of these platforms may focus on ESG integration, while others emphasize tax optimization or sector-specific tailoring. Navigating the overall investment landscape can be overwhelming, which is why working with an experienced advisor can be a crucial advantage.

At HUDSONPOINT capital, we help clients evaluate strategies, compare opportunities, and choose solutions that align precisely with their goals and constraints. If you’re looking for the best platform for direct indexing or need help comparing your options, we are here to guide you through the decision-making process.

The opinions expressed are those of HUDSONPOINT capital and not those of Arete Wealth.

Please note that any investment involves risk including loss of principal. This is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation of any products or services. Opinions are subject to change with market conditions. The views and strategies may not be suitable for all investors and are not intended to be relied on for legal or tax advice.

Securities offered through Arete Wealth Management, LLC, members FINRA and SIPC. Investment advisory services offered through Arete Wealth Advisors, LLC an SEC registered investment advisory firm.

.png)

.png)

.png)